As of October of 2022, UCAP is the ONLY organization to present an appraisal/ real estate course (4 hrs.) about these issues.

Research Summary. Demographics estimates and statistics for real estate appraisers in the United States verified against BLS, the US Census, and current job openings data for accuracy. After extensive research and analysis, the data science team found that:

- There are over 33,548 real estate appraisers currently employed in the United States.

- 33.5% of all real estate appraisers are women, while 66.5% are men.

- The average age of an employed real estate appraiser is 50 years old.

- The most common ethnicity of real estate appraisers is White (85.1%), followed by Hispanic or Latino (8.9%), Black or African American less than (2%), and Asian (2.9%).

- In 2021, women earned 93% of what men earned.

- 7% of all real estate appraisers are LGBT.

- Real estate appraisers are 55% more likely to work at private companies in comparison to public companies.

The bias in today’s appraisal system goes back to the 1930s and the now-notorious practice of redlining. After being elected President Roosevelt promise to restore the economy. His administration argued a key component should be enabling more middle-class families to become homeowners. To do this, they fundamentally restructured the housing market,” explains the appraisal bias study’s co-author Elizabeth Korver-Glenn, assistant professor of sociology at the University of New Mexico.

It is improper to base a conclusion or opinion of value, or a conclusion with respect to neighborhood trends, upon stereotyped or biased presumptions relating to race, color, religion, sex, or national origin or upon unsupported presumptions relating to the effective age or remaining life of the property being appraised or the life expectancy of the neighborhood in which it is located.

For the dataset, 21,095 appraisers submitted reports for Black and White buyers—of them 934 appraisers submitted enough appraisals for each group to be deemed statistically significant. Of the 934 appraisers, about 6% had appraisal reports that showed a Black versus White gap of 10%. This differs in the case of unbiased appraisals, where about half of the appraisers would show negative estimated gaps. The data is similar for the Latino versus White demographic with 18,905 appraisers submitting reports for both groups and 1,560 submitting enough data to be deemed significant.

* If you feel that this has happened to, you please contact us. *

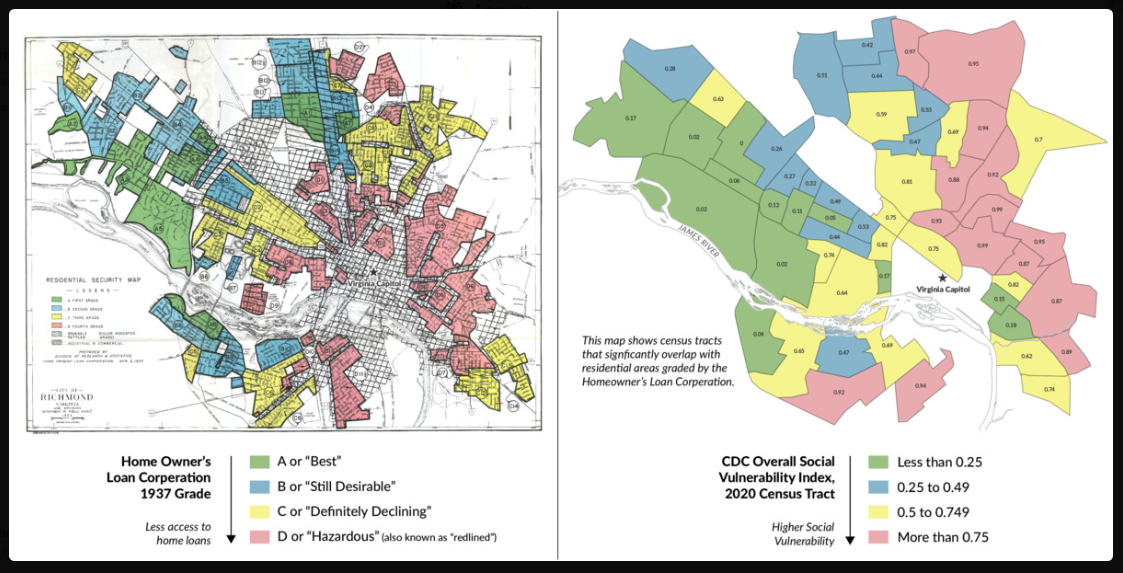

Appraisal bias has its roots in the 1930s, when the Home Owners’ Loan Corporation (HOLC) developed color-coded “Residential Security” maps to assess lending risk in different

Neighborhoods27. These maps incorporated racial and ethnic information to determine “credit worthiness,” with areas predominantly housing Black and other minority households often designated as high-risk.

1934, the Federal Housing Administration (FHA) was established and adopted similar discriminatory practices. The FHA created “redlining maps” that deemed certain areas, primarily those with Black and Hispanic residents, too risky for federal mortgage insurance. This practice institutionalized racial discrimination in lending on a federal level.

The FHA’s underwriting standards In explicitly favored loans in white-only neighborhoods and new suburban developments over older urban properties. This approach not only perpetuated racial segregation but also contributed to urban decay and the growth of predominantly white suburbs.

These discriminatory practices had long-lasting effects on housing and wealth accumulation for minority communities, with impacts still evident today. Although officially banned by the Fair Housing Act over 50 years ago, the legacy of these policies continues to shape urban landscapes and economic opportunities.